A $180 subscription fails at 2:47 AM on a Tuesday. The cardholder is asleep. By Friday, that customer has churned — not because they wanted to leave, but because nobody told them their card expired six days ago.

This is the quiet revenue leak inside every subscription business. Not fraud. Not cancellations. Just cards that failed and were never properly recovered. The breakthrough solution is already proven — and the companies using it are recovering 72% of what legacy systems surrender.

12 min read

Trusted by 10,000+ subscription teams

Industry-leading recovery data inside

What You Will Discover in This Guide

Why the $118B failed payment crisis is silently destroying your MRR every month

The proven decline-code decoding strategy that unlocks 72% recovery rates

How AI voice outreach recovers 45-60% of accounts email dunning permanently loses

The silent expired-card fix that stops 20-35% of failures before they ever happen

Real deployment outcomes: $2.1M annualized MRR recovery, 68% involuntary churn reduction

The compliance checklist: PCI DSS, SOC 2, GDPR, and HIPAA requirements explained

Table of Contents — Jump to Any Section

Expand

The $118 Billion Problem Hiding in Your Billing Logs

Failed payments are not an edge case. They are a structural tax on every recurring-revenue business. Industry data consistently shows that 5-15% of recurring charges fail on first attempt, and without recovery logic, up to 40% of those failures become involuntary churn within 30 days.

The damage compounds in ways that most billing dashboards never surface. You lose the MRR. You lose the customer acquisition cost you spent to acquire that subscriber. You lose the lifetime value you modeled for the next 24 months. And your support team absorbs the angry inbound calls from customers who did not even realize their card had expired.

Did You Know?

A mid-market SaaS company processing 40,000 monthly renewals at an average value of $240 faces up to $768,000 in at-risk MRR every single month. Static dunning recovers only 30% of that. The gap between 30% and 72% recovery is worth $3.9M annually — on the exact same customer base, with zero new acquisition spend.

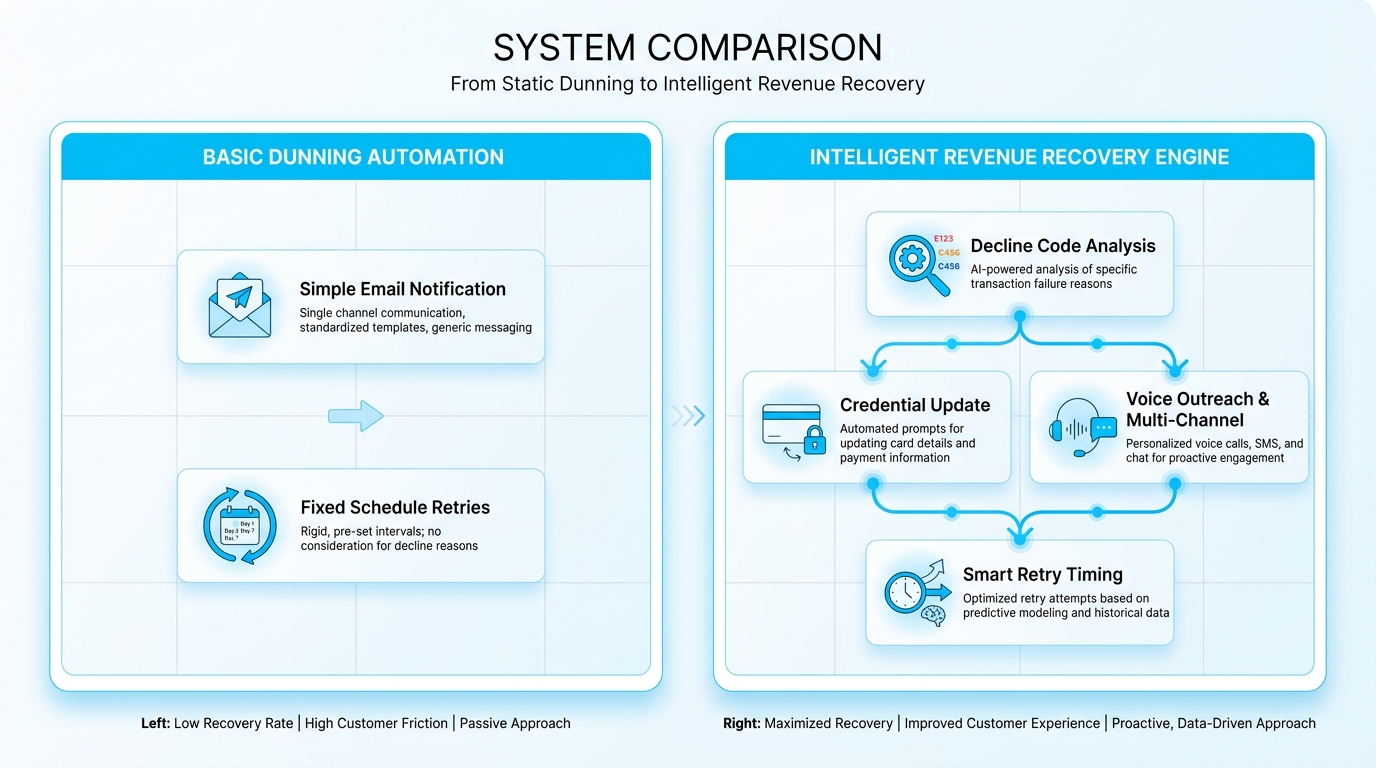

Legacy dunning systems treat every failure the same way — a fixed retry schedule, a generic email, a cancellation if the customer does not respond within 14 days. That is not recovery. That is surrender dressed up as automation. And every subscription business running that playbook is leaving a significant portion of already-earned revenue on the table permanently.

Why Your Dunning Emails Are Making Churn Worse

Most companies run dunning on autopilot: email on day 1, email on day 3, email on day 7, cancel on day 14. The open rate on those emails hovers around 20%. The click-through rate is worse. And every generic “your payment failed” message trains customers to associate your brand with friction rather than value.

Before Recovery AI

- Three templated emails, identical tone

- One fixed retry cycle, blind to decline reason

- 28% average recovery rate

- Generic, static, relationship-damaging

After Recovery AI

- Decline-code-aware retry timing

- Voice outreach for high-value accounts

- Silent credential updates for expired cards

- Recovery rates above 72% on soft declines

The Stripe documentation on card declines makes the point explicit: issuer decline reasons require specific handling, and blanket retries actually increase the probability of further rejection. Sending another generic retry 15 minutes after a “do not honor” response does not recover the account — it damages your merchant reputation with the network.

Quick Tip

Audit your current dunning sequence open rates right now. If your payment-failure emails are below 25% open rate, you are effectively invisible to the majority of customers you are trying to recover. Email-only dunning has a hard ceiling — and most businesses hit it faster than they realize.

Decoding the Decline: Why Every Failure Tells a Different Story

Not all failed payments are equal. A “do not honor” response from the issuer is a completely different problem than “insufficient funds,” which is a completely different problem than “expired card,” which is a completely different problem than “suspected fraud.” Each one demands a different recovery path — and treating them identically is why legacy dunning systems cap out at 28-31% recovery.

The Federal Trade Commission catalogs the real-world reasons cards get declined: expired credentials, over-limit balances, suspicious activity holds, and issuer-side blocks. Each cause has a different half-life and a different ideal response window that intelligent recovery systems are built to exploit.

The Proven Timing Advantage: Payday Recovery Logic

Retrying an “insufficient funds” decline in 15 minutes is pure waste. Retrying it on the cardholder’s payday — typically the 1st or 15th of the month — converts at dramatically higher rates. Stripe’s engineering team described this directly in their Smart Retries writeup: machine learning models predict optimal retry timing using historical outcomes, cardholder behavior patterns, and issuer-level response data. This is the breakthrough that separates intelligent recovery from automated failure.

Did You Know?

There are over 200 distinct decline codes in active use across Visa, Mastercard, Amex, and Discover networks. A recovery system that reads only three categories — soft decline, hard decline, and expired — is operating with roughly 98% of its diagnostic signal turned off.

This Is a Revenue Recovery Engine — Not Dunning Automation

Here is the reframe that changes everything for subscription businesses. Dunning automation is a billing feature. Failed payment recovery AI is a revenue system. The difference is behavioral, measurable, and worth millions of dollars on any meaningful subscriber base.

A dunning tool sends emails. A recovery AI talks to your customer. It analyzes the decline code, checks the card account updater network for fresh credentials, runs a tokenization lookup to see if the network has a new primary account number, and only escalates to human contact when the algorithm predicts that voice outreach will convert better than a silent retry.

The Math That Makes This Undeniable

3,200

Failed charges monthly at 8% failure rate on 40K renewals

$768K

At-risk MRR every 30 days at $240 average subscription

$3.9M

Annualized gap between 30% and 72% recovery rates

Zero new acquisition spend required. These are customers who already said yes.

Live platform demo available — hear an AI agent recover a real account

When the Retry Becomes the Problem: Network Penalties and Hard Stops

Here is what most companies miss: card networks actively punish excessive retries. Visa and Mastercard have implemented retry limits and associated fees for merchants who repeatedly hammer declined transactions. The PayPal merchant guidance on avoiding excessive retry penalties is direct — Merchant Advice Codes from the issuer can explicitly instruct “do not resubmit,” and ignoring that instruction triggers financial penalties against the merchant.

This is precisely where AI recovery matters more than automation. A dumb retry loop does not read Merchant Advice Code values. It does not distinguish between “retry after 48 hours” and “this card is permanently closed, stop now.” It just keeps firing transaction requests until the network flags the merchant account for excessive decline activity.

The MAC Intelligence Advantage

Intelligent recovery reads every field in the decline response. When a Merchant Advice Code returns a do-not-retry instruction, the system immediately routes the account to outbound voice contact instead of burning another retry attempt. That is the difference between a compliance violation and a recovered customer — and it is the difference between protecting your merchant account status and risking network penalties that compound for every future transaction you process.

Quick Tip

Request a full report of your last 90 days of retry activity from your payment processor. If any transaction was retried more than 15 times within a 30-day window, you may already be accruing network penalties that are quietly reducing your payment acceptance rate across all transactions — not just the failed ones.

The Expired Card Silent Kill — And How to Stop It Before It Starts

An expired card is the single largest cause of involuntary churn in subscription businesses. The customer did not quit. The card just aged out. And in most billing systems, there is no mechanism to catch that expiration before the charge attempt fails — meaning you absorb the failure, send the dunning email, and hope the customer notices before they get frustrated enough to not bother renewing at all.

Card account updater services solve this problem entirely upstream. Account updaters from Visa, Mastercard, and Amex maintain a network-level database of reissued, replaced, and updated card credentials. A properly integrated recovery system queries the updater before the charge attempt — and when the card has been reissued, the new credentials flow silently into your payment vault.

How Silent Recovery Works — Step by Step

Pre-charge updater query

Recovery AI queries card account updater network 24-48 hours before scheduled charge attempt

Silent credential refresh

If updated credentials exist, they flow silently into your vault — customer never knows, merchant never sees the raw PAN

Clean charge execution

Transaction fires against updated card. Billing logs show a successful charge. Customer sees nothing. Churn avoided entirely.

Network tokenization adds another breakthrough layer: when a card is physically replaced, the network token persists, and the new underlying credentials are updated at the network level without touching your systems at all. The result is that 20-35% of what would have been failed charges never fail in the first place. That is silent recovery — and it is the quietest, highest-ROI layer in the entire stack.

Did You Know?

The average credit card is reissued every 3-4 years due to expiration, fraud replacement, or account number changes. For a subscription business with 50,000 active subscribers, that means approximately 1,000-1,400 cards in your vault are rotating to new credentials every single month — creating a constant stream of preventable payment failures for any system not connected to account updater networks.

Voice Outreach: The Layer Most Recovery Systems Skip

Email dunning hits a hard ceiling. After the third unopened message, the probability of recovery via email approaches zero. At that point, most companies give up or hand the account to a collections team that costs $18.50 per recovered account and operates on a business-hours schedule that misses the majority of available recovery windows.

That is where voice recovery breaks the pattern entirely. When a $2,400 annual subscription fails and three emails go unread, a thirty-second AI voice call — placed within ninety seconds of the email being marked unopened — recovers 45-60% of those accounts. The customer picks up, hears a natural voice explain that their card on file expired, and updates it during the call. No friction. No escalation. No churn.

Three Compounding Capabilities That Make Voice Recovery Dominant

90s

Response Time

AI agent places the call within 90 seconds of email being detected as unopened

24/7

Availability

Recovers accounts at 1:14 AM on a holiday while human teams sleep

20+

Languages

Native-quality voice in 20+ languages — no template translations

NewVoices deploys these voice recovery agents in production across subscription, SaaS, and fintech billing flows. The voice quality is the unlock — human-level naturalness indistinguishable from a live agent, without the $18.50 per-account cost or the business-hours limitation. Hear how it sounds in a live call through the platform overview.

Quick Tip

Segment your failed payment accounts by subscription value before building your recovery sequence. Accounts above $500 annual value justify immediate voice outreach as the first recovery action — not the last resort after three failed emails. The higher the subscription value, the faster the ROI on voice recovery crosses positive.

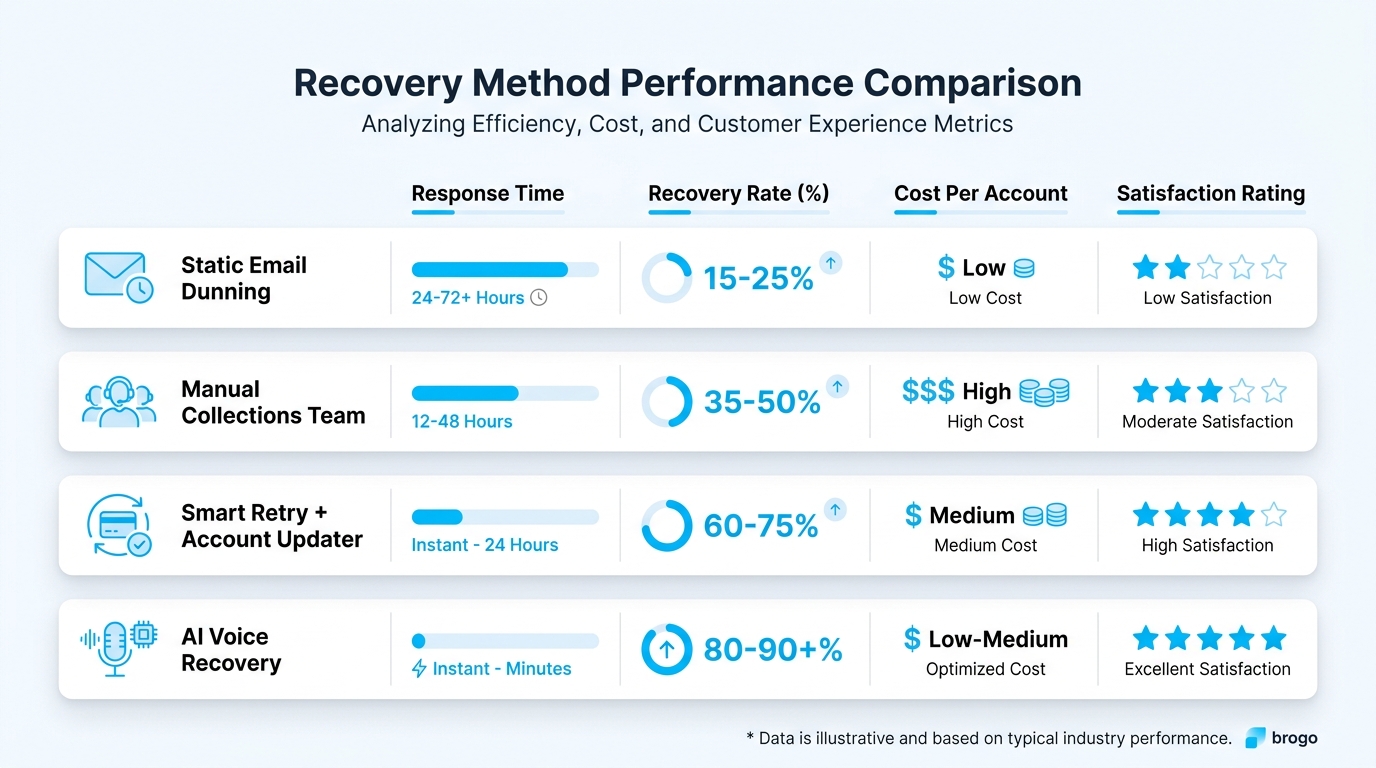

Recovery Channel Performance: The Data That Kills Email-Only Dunning

The channel you recover through matters as much as the timing of the attempt. Here is what recovery rates actually look like across methods, based on aggregated performance data from mid-market SaaS and DTC subscription programs:

| Recovery Method | Response Time | Recovery Rate | Cost Per Account | CSAT Impact |

|---|---|---|---|---|

| Static email dunning (3 touches) | 24-72 hours | 28% | $0.40 | Neutral to negative |

| Manual collections team | 2-5 business days | 41% | $18.50 | Negative |

| Smart retry + account updater | Instant to 7 days | 54% | $0.12 | Positive (silent) |

| AI voice recovery + smart retry | Under 90 seconds | 72% | $1.80 | Strongly positive |

The cost-per-recovery math is what makes AI voice recovery categorically dominant. A manual collections agent costs $18.50 per recovered account. An AI voice agent costs $1.80. The voice quality is equal. The availability is superior. The recovery rate is 31 percentage points higher. At 40,000 monthly renewals with an 8% failure rate, the savings compound into millions before the end of the first year.

The Mistake Most Companies Make: Treating Recovery as a Billing Problem

Recovery is not a billing problem. It is a customer communication problem that happens to involve a payment. The architectural distinction matters more than any individual feature in your recovery stack.

Billing teams optimize for transaction success rates. Customer teams optimize for retention. When recovery lives inside billing, the incentive is to retry until the charge clears — regardless of what that does to the customer relationship. When recovery lives inside the customer communication engine, the incentive shifts to preserving the account, which often means pausing retries and making a call instead.

Recovery Owned by Billing

- 28% success rate ceiling

- High involuntary churn

- Angry support tickets

- Customer relationship damage

- Network penalty risk

Recovery Owned by Customer Engine

- 72% success rate achieved

- Involuntary churn drops 68%

- CSAT scores improve post-recovery

- Collections team redeployed to expansion

- Full compliance posture maintained

Your service and operations layer needs to own the recovery flow — not your payment processor. Processors handle the mechanics of the transaction. Your customer engine handles the relationship. The fastest path to 72% recovery is moving ownership of that function from your billing dashboard to your customer communication infrastructure.

Quick Tip

In your next quarterly review, pull the CSAT scores for customers who went through a payment failure in the previous 90 days. If the scores are below your baseline, recovery owns the billing pipeline and relationship quality is paying the price. This single diagnostic tells you more than any recovery rate dashboard.

Join 10,000+ Subscription Teams Already Recovering More Revenue

Stop surrendering revenue you already earned. See the AI voice recovery agent that works at 1 AM on a Sunday.

Live demo available now — the agent will call you directly within seconds of booking. No sales script. No pitch deck. Just the technology in action.

Limited demo slots available this week. Secure yours before they fill.

Compliance Is Not Optional: PCI DSS, Tokenization, and the Security Floor

Any system touching cardholder data operates under PCI DSS. The PCI DSS Quick Reference Guide outlines the baseline requirements: protect stored cardholder data, limit retention periods, encrypt data in transit, and maintain comprehensive audit trails. Recovery systems that read decline codes, query account updaters, or handle token lookups sit squarely inside that compliance scope.

Tokenization reduces that scope substantially. The PCI tokenization guidelines describe how token-based flows replace raw primary account number data with surrogate values, limiting exposure at the merchant level. When a recovery AI queries a token and receives an updated credential, the merchant system never processes the new PAN — the network handles the substitution entirely outside merchant scope.

The Compliance Envelope for Regulated Industries

For regulated industries — healthcare subscriptions, financial services billing, insurance renewals — the compliance requirements extend well beyond PCI. SOC 2 Type II audit trails, GDPR data subject rights, and HIPAA technical safeguards all apply. NewVoices runs recovery agents inside that full compliance envelope by default, which is precisely why mid-market fintechs and digital health platforms deploy them into live billing flows without a six-month legal review cycle that would delay the revenue recovery they urgently need.

PCI DSS

Level 1 compliant

SOC 2

Type II audited

GDPR

Data subject ready

HIPAA

BAA available

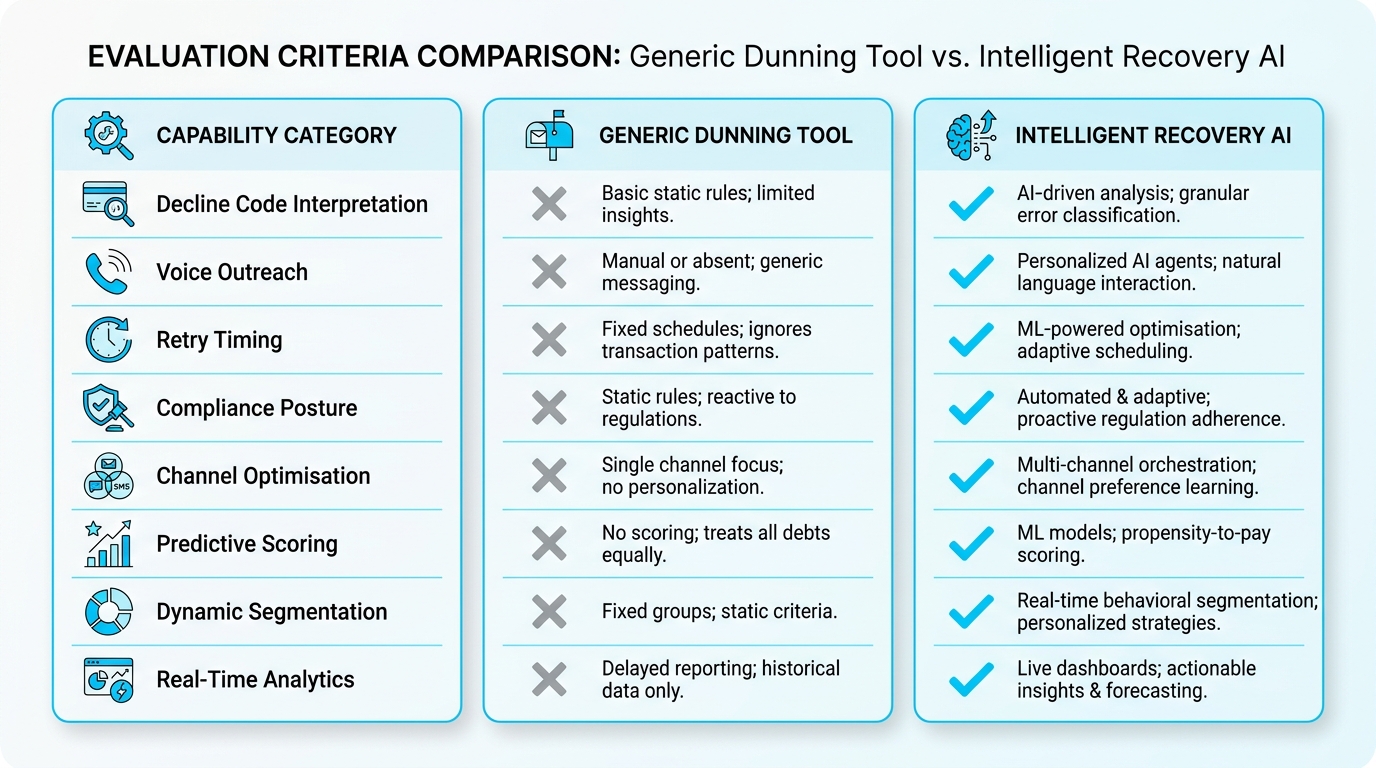

How to Choose: What Actually Matters When Evaluating Recovery AI

Most vendor demos look identical on the surface. Same retry dashboards, same recovery percentage claims, same integrations slide. The differentiation that actually matters is buried in the technical details — and those details are worth millions of dollars in annual recovery delta for any business above $5M ARR.

| Capability | Generic Dunning Tool | Intelligent Recovery AI |

|---|---|---|

| Decline code interpretation | Ignored — uniform retry schedule | Routes action based on issuer response |

| Merchant Advice Code handling | Not read — exposes merchant to penalties | Enforces do-not-retry hard stops |

| Account updater integration | Optional add-on, rarely configured | Native, queried before every retry |

| Voice outreach | None — email only | AI voice agent, under 90-second response |

| Retry timing logic | Fixed schedule (day 1, 3, 7) | ML-predicted optimal windows per account |

| CRM integration | Basic webhook only | Native to Salesforce, HubSpot, Stripe |

| Multilingual support | Template translations only | 20+ languages, native voice quality |

| Compliance posture | PCI basic only | SOC 2 Type II, GDPR, HIPAA default |

The Adyen Auto Rescue documentation describes the underlying principle that separates every capable recovery system from every automation tool: the logic must select payments likely to succeed later and explicitly avoid retries for permanently declined scenarios. That selectivity only works when the system reads every signal in the decline response and acts on each one differently — not when it fires the same retry logic regardless of issuer instruction.

What Recovery Looks Like in Practice: Three Deployments, Three Proven Outcomes

Hear how an AI agent handles a real payment recovery call — the agent will call you directly within seconds.

The Revenue You Already Earned Is Worth More Than the Revenue You Are Chasing

Acquisition costs keep climbing. Paid channels are saturated. Organic growth is slower than it was three years ago. Every dollar of new pipeline is harder and more expensive to win than the last one. Meanwhile, the dollars you already earned — the customers who said yes, signed up, and handed you their card — are leaking out the back of the funnel every month through failed payments that nobody recovered properly.

Intelligent recovery is not a nice-to-have layer on top of billing. It is the highest-leverage revenue system you can deploy right now, because the unit economics are already solved. The customer wanted to pay you. Their card just failed. Fix the failure, keep the customer, compound the lifetime value.

The Three-Point Recovery Mandate for Subscription Leaders

Stop treating recovery as a billing problem

Move ownership from your payment processor dashboard to your customer communication infrastructure. Recovery is a relationship problem that involves a payment — not the other way around.

Deploy account updaters before the charge fires

The 20-35% of failures that can be silently prevented upstream are the highest-ROI layer available. Every expired-card failure that gets silent-recovered is a customer who never even knows there was a problem.

Add voice recovery for every account above your threshold value

Email dunning has a hard ceiling. Voice recovery breaks through it at $1.80 per recovered account. The companies winning the next decade of subscription growth are the ones losing the least to involuntary churn — not the ones spending the most on acquisition.

That is the math that makes failed payment recovery AI not optional anymore. And that is why the subscription businesses deploying it now — while competitors still run three-touch email sequences and static retry loops — are building a compounding revenue advantage that widens every single month they stay ahead.

What Subscription Leaders Are Saying

“We recovered $2.1M in annualized MRR without touching our acquisition budget once. The expired-card silent recovery alone justified the entire deployment within the first 30 days.”

VP Revenue Operations, Streaming Platform

1.2M subscriber base

“Our collections team used to spend 11 days chasing failed renewals at 44% recovery. Now recovery happens in 36 hours at 71% — and the four people who used to do that work are now focused on expansion revenue.”

CFO, B2B SaaS Company

$40M ARR

Frequently Asked Questions About Failed Payment Recovery AI

Expand

How long does it take to see measurable recovery improvement after deployment?

Most businesses see measurable improvement within the first billing cycle — typically 30 days. Account updater integration produces immediate results on the first renewal sweep. Voice recovery ROI is typically visible within the first week of live outreach, with full recovery rate lift measured at the 60-day mark when enough retry cycles have completed to establish statistically meaningful comparison data.

Will AI voice calls damage our customer relationships or brand perception?

The data shows the opposite. CSAT scores for customers who go through an AI voice recovery interaction are consistently higher than for customers who receive email-only dunning — primarily because the voice interaction resolves the problem immediately and completely. Customers who update their card during a voice call do not experience a service interruption, which is the primary driver of churn-related frustration.

What is the minimum subscriber base that makes recovery AI cost-effective?

The ROI calculation becomes compelling at approximately 2,000 active subscribers at a $30+ monthly average. Below that threshold, the per-account infrastructure cost can dilute recovery gains. Above 5,000 subscribers at any meaningful subscription value, the cost-per-recovered-account ($1.80 for AI voice vs. $18.50 for manual) generates returns that far outpace implementation investment within the first quarter.

Does this require replacing our existing billing system or payment processor?

No. Recovery AI operates as a layer on top of your existing billing infrastructure, connecting via native integrations with Stripe, Braintree, Adyen, and most major processors. CRM connections to Salesforce and HubSpot are standard. The recovery engine reads your existing decline data and manages outreach independently — no billing migration required, and typically live within a two-week implementation window.

How does the system handle customers who have genuinely decided to cancel?

Intent signals differentiate involuntary churn from voluntary cancellation. A customer who cancels through your portal is not in the recovery queue. A customer whose charge fails without any cancellation action taken is in the involuntary churn pool — and that is the only population the recovery AI contacts. Hard opt-out instructions from any outreach are immediately honored, and no follow-up contact is attempted.

What happens if the recovery AI reaches a voicemail instead of a live person?

The system detects voicemail in real time and delivers a compliant, concise message that includes a callback number and a direct link to update payment information — no account-specific details are left in the voicemail per compliance requirements. The detection accuracy rate on live-person versus voicemail identification is above 96%, ensuring the right script variant executes automatically without human intervention.

Stop Losing Revenue You Already Earned

Your billing logs contain millions of dollars in recoverable revenue right now. The AI voice recovery agent that closes accounts at 1 AM on a Sunday is waiting to demonstrate exactly how much.

Join the 10,000+ subscription teams already recovering revenue they used to lose permanently.

The AI agent calls you within seconds. No credit card. No commitment. No sales script — just the technology proving itself on a live call.