One unlawful automated call can cost $1,000 in statutory damages under the FDCPA — multiply that across thousands of accounts and your AI becomes a lawsuit factory before anyone notices the pattern.

The breakthrough that changes everything is not faster dialing. It is compliance-native AI that physically cannot break the rules — because the regulatory guardrails are baked into the infrastructure from day one, not bolted on after a cease-and-desist letter arrives.

What You Will Gain From This Guide

Eliminate Compliance Exposure

Proven architecture that reduces post-revocation contacts to under 0.02%

Recover More Revenue

34% lift in delinquent account recovery with compliant 24/7 outreach

Survive Any Audit

Immutable audit trails exportable in under 4 hours vs. 6-week scrambles

Scale Without Legal Risk

Hard-coded regulatory caps that make FDCPA violations physically impossible

What Compliant Debt Collection AI Actually Means — And Why the Definition Matters

Compliant debt collection AI is not a chatbot with a legal disclaimer pinned to its prompt. It is a purpose-built voice and messaging system that enforces every rule in the FDCPA, Regulation F, and TCPA at the infrastructure layer — not the conversation layer.

The difference matters more than most operations realize. A generic AI agent can be told to follow the rules. A regulated collection AI cannot break them, because the rails are built into the system: frequency caps enforced by the dialer, validation notices triggered before substantive communication, opt-outs processed in real time across every channel simultaneously.

NewVoices operates exclusively in this second category. Every call, SMS, and email passes through a compliance layer before it reaches a consumer — and every interaction leaves a timestamped, audit-ready record that can be exported to any e-discovery platform regulators already recognize.

Quick Tip

Before evaluating any AI collection platform, ask the vendor one question: does your compliance enforcement happen at the infrastructure layer, or at the conversation layer? The answer will tell you everything you need to know about your actual exposure.

Your Collections Floor at 9:47 PM — The Revenue Window Legacy Systems Cannot Reach

Your collections floor closed three hours ago. A consumer logs into their account portal at 9:47 PM, wants to set up a payment plan, and has exactly twelve minutes before their toddler wakes up. In a traditional operation, that contact window is dead. The lead gets a voicemail in the morning. The promise-to-pay never materializes.

With a compliant AI voice agent running, the consumer is on a live call in under three seconds, validated against the account record, walked through an FDCPA-compliant disclosure, and closed on a payment plan before the toddler cries. That contact happens without a single human agent on shift.

Did You Know?

Studies consistently show that consumers are most likely to resolve delinquent accounts in the evening hours — precisely when most collections operations have already closed for the day. The operations recovering the most revenue are the ones operating compliantly around the clock, not the ones with the most daytime agents.

NewVoices deployments report an average 34% increase in delinquent account recovery — driven largely by after-hours contact windows.

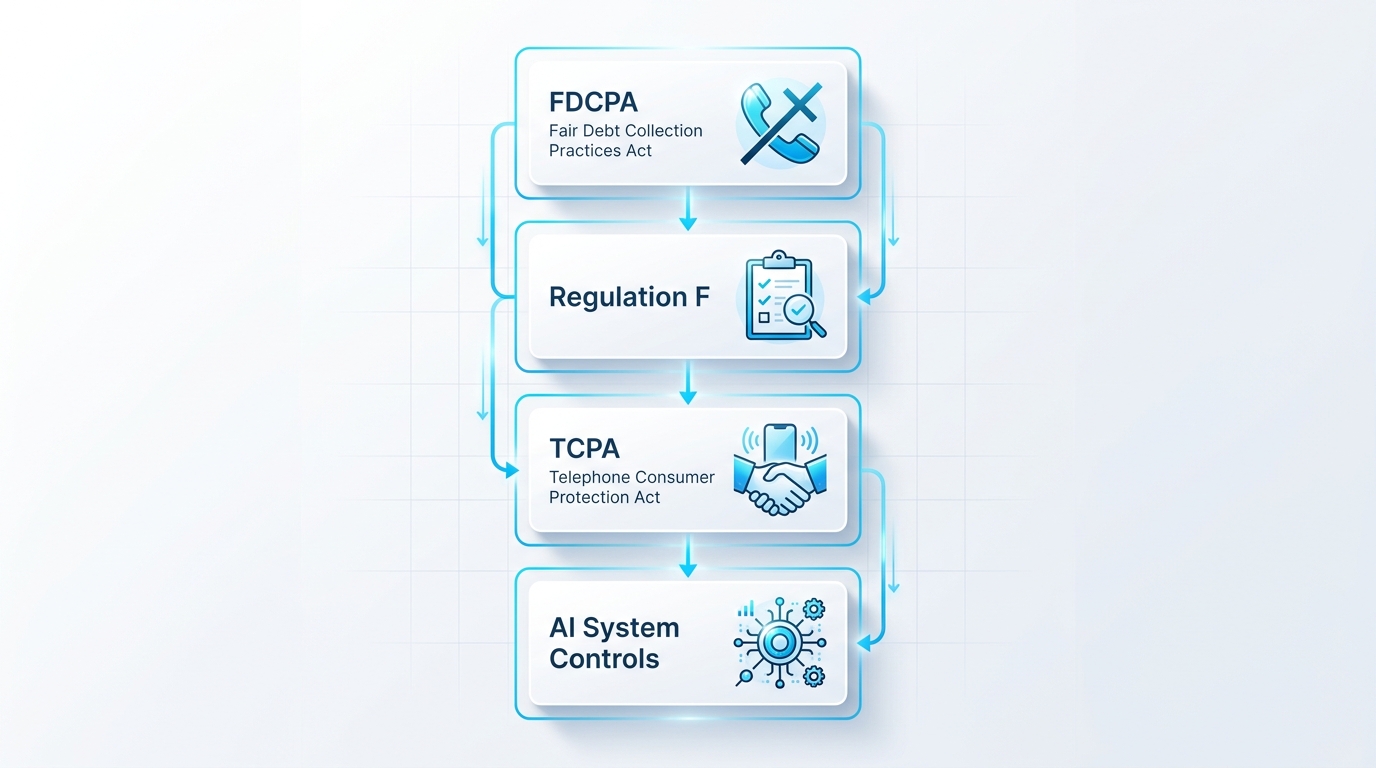

The Proven Regulatory Stack: FDCPA, Reg F, and TCPA Unified in One Workflow

Three distinct federal frameworks govern modern debt collection communications, and a compliant system must satisfy all of them simultaneously without any gaps at the seams.

The FDCPA sets the foundational rules: no harassment, no false representations, strict limits on third-party contact, mandatory disclosures. 15 U.S.C. § 1692c governs when and how consumers can be contacted and enforces cease-communication requests with immediate legal effect.

Regulation F, issued by the CFPB, translates those rules into operational specifics — validation notice content, call frequency presumptions (the seven-in-seven rule), electronic communication consent, and opt-out mechanics that must work across every channel. TCPA layers on top for any automated outreach, and as of February 2024, the FCC explicitly classified AI-generated voices as artificial voices under TCPA — meaning prior express consent rules now apply to every AI collection call without exception.

Validation Notices: The Quiet Place Where Most Systems Fail — And Why Yours Cannot

12 CFR § 1006.34 requires a validation notice containing specific itemized information — the debt amount, itemization date, creditor name, and consumer rights — delivered in a form the consumer actually receives and can verify.

Generic AI solutions treat this as a document to email and move on. Compliant debt collection AI treats it as an absolute gate. No substantive collection conversation begins until the notice is delivered, the delivery is logged with a timestamp, and the five-day window is individually tracked per account across the entire portfolio.

Proven Social Proof — Real Client Outcome

“A NewVoices deployment at a mid-market receivables firm cut validation notice disputes by 78% in the first quarter — not because the notices changed, but because delivery became provable down to the millisecond.”

Limited Availability — Compliance Audits Book Fast

See How Your Current Stack Compares to a Compliance-Native System

Join 500+ collections operations that have already eliminated their compliance exposure with NewVoices. Schedule your free architecture review before slots fill.

Get Your Free Compliance Architecture Review

No commitment required. SOC 2 Type II certified. HIPAA and GDPR compliant.

Why Faster Response Times Alone Will Turn Your Collections Operation Into a Liability Engine

The industry loves to talk about speed. Answer every call in under three seconds. Dial every account within the hour. Send every SMS the moment a consumer becomes reachable. Speed is seductive — and without compliance architecture underneath it, it is a guaranteed path to class-action exposure.

An operation that dials 10,000 accounts per day at peak efficiency but breaches Regulation F’s frequency presumptions on just 4% of them is generating 400 potential violations daily. At statutory minimums, that calculates to $400,000 in exposure per day — before class certification multiplies it across an entire portfolio.

Quick Tip — The Real Metric That Protects Revenue

Stop measuring response time alone. Start measuring compliant response time. The CFPB’s official interpretation of § 1006.14 makes the frequency math unforgiving: seven calls in seven days triggers a presumption of harassment regardless of whether a conversation occurred. Regulated collection AI enforces those limits at the system level — a compliance-native AI cannot exceed a cap it does not have permission to exceed.

Collections Compliance Is an Air Traffic Control Problem — And Your Agents Should Not Be the Last Defense

Consider how air traffic control works. Thousands of aircraft, dozens of airports, hundreds of controllers, one rulebook. The system does not rely on individual pilots remembering every regulation. It relies on layered controls — transponders, collision avoidance systems, controlled airspace, automated separation — that make most violations physically impossible even if a pilot forgets the rule.

Debt collection at scale requires the same architecture. Your agents — human or AI — should not be the last line of defense against a TCPA violation. The dialer should refuse to place the call. The SMS gateway should refuse to send the message. The email system should refuse to attempt delivery to an address that revoked consent six weeks ago.

This is how NewVoices is built. Compliance is not a training module for the AI agent. It is the runway the agent taxis on. The NIST AI Risk Management Framework calls this approach governance as a foundational function — and it is the proven difference between an AI that behaves well under ideal conditions and an AI that cannot misbehave under any conditions.

Consent, Revocation, and the Unified Opt-Out Ledger That Eliminates Your Biggest Exposure Window

12 CFR § 1006.6 defines how electronic communications must operate in collections. Clear consent. Reasonable and simple opt-out procedures. Honoring the request without delay. The phrase without delay is where most systems collapse — and where most violations originate.

Here is the failure pattern that generates hundreds of TCPA claims every year: A consumer texts STOP to an SMS campaign. The SMS gateway registers the opt-out. But the voice dialer — running on a separate infrastructure stack — still has that phone number queued for a call in forty minutes. The call goes out. The violation is recorded in your own logs. The complaint is filed the next morning.

A compliant debt collection AI operates on a unified consent ledger. The moment a revocation lands on any channel — voice, SMS, email, web portal, or live agent transfer — it propagates across every outreach system in under a minute. No queued calls. No scheduled texts. No email drips. The FCC’s 2015 TCPA Omnibus Ruling established that consumers may revoke consent by any reasonable means — which means your system must recognize all of them simultaneously.

Quick Tip — Audit Your Revocation Propagation Today

Run a simple test: send a STOP text to your SMS number at 2 PM and check whether your voice dialer still has that number queued for an outbound call at 2:45 PM. If the answer is yes, you are generating live violations at scale right now.

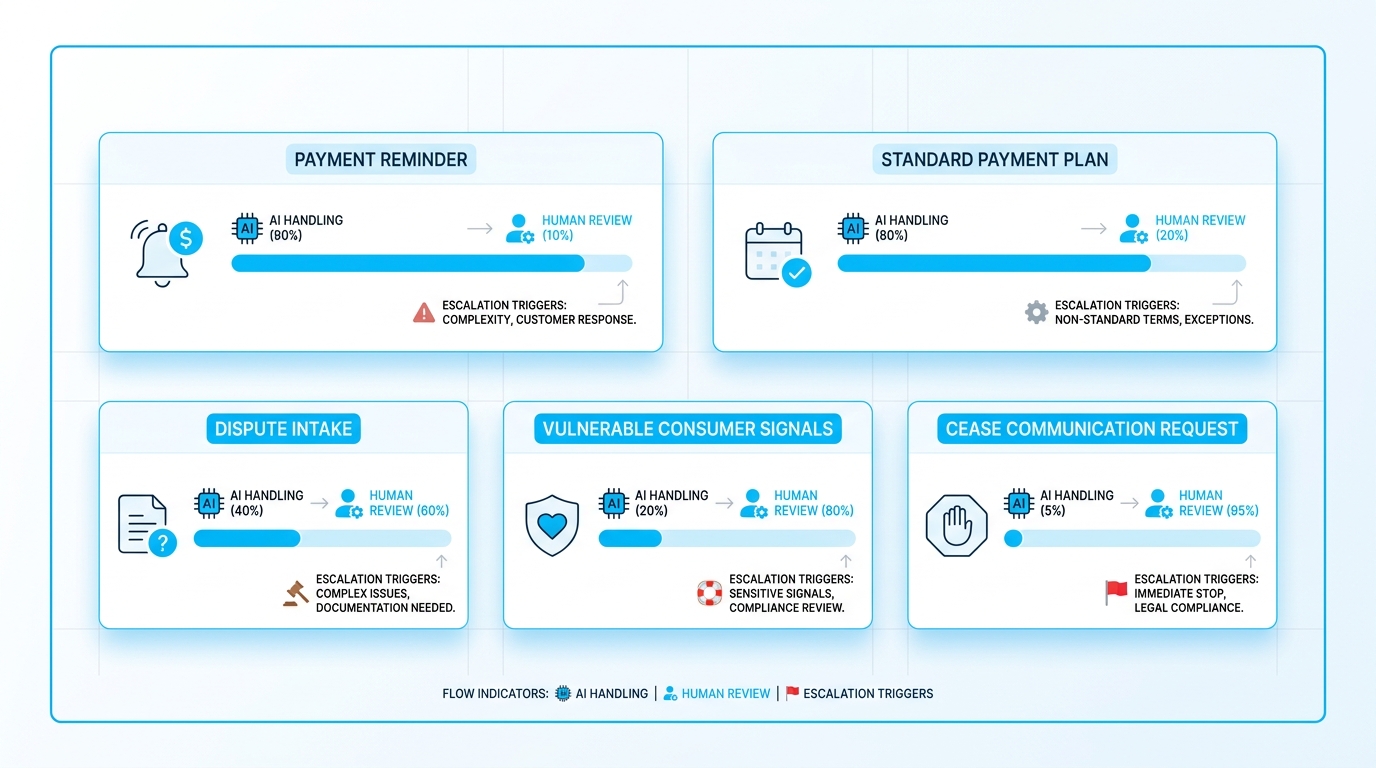

Human Oversight: The Non-Negotiable Layer That Makes Automation Legally Defensible

Human-in-the-loop checkpoints ensure compliance at every critical decision boundary — protecting both consumers and your operation from AI acting beyond its authority.

An AI that runs collections without human oversight is not an efficiency gain. It is a liability engine with no circuit breaker. This is not a contradiction of automation — it is the architecture that makes automation legally defensible and operationally scalable at the same time.

Every NewVoices deployment in a regulated vertical operates with human-in-the-loop checkpoints at specific decision boundaries: payment plan modifications beyond pre-approved terms, disputed account escalations, legally sensitive consumer statements, and vulnerable consumer identifications. The AI handles the volume. The human handles the judgment that no model should exercise alone.

Audit Trails That Survive Litigation — The Difference Between a Defense and a Seven-Figure Settlement

A regional healthcare receivables company faced a TCPA class action covering 18 months of outbound calls. The plaintiffs alleged hundreds of post-revocation contacts. The defense took four weeks to assemble — because the company’s audit logs were scattered across three vendors, two CRMs, and a dialer that overwrote call detail records after 90 days. The case settled for seven figures before discovery finished.

Compare that to an audit trail designed for compliance from day one: every call recorded and transcribed, every consent state timestamped with immutable precision, every revocation propagation logged across all channels, and every AI decision explainable with the underlying policy rule that triggered it — exported to any e-discovery platform in under four hours.

The NIST AI RMF treats documentation and traceability as core governance requirements — not optional hygiene. NewVoices retains full interaction records with immutable hashing, exportable to any e-discovery platform in a format regulators already recognize. Legal defensibility is not a feature of the platform. It is the foundational product.

Did You Know?

The average TCPA class action settlement in debt collection now exceeds $3.8 million — and the average time from initial complaint to settlement is 22 months of legal overhead. A compliance-native audit infrastructure does not just reduce violations. It dramatically shortens the resolution timeline when disputes arise because the evidence is already organized, timestamped, and ready.

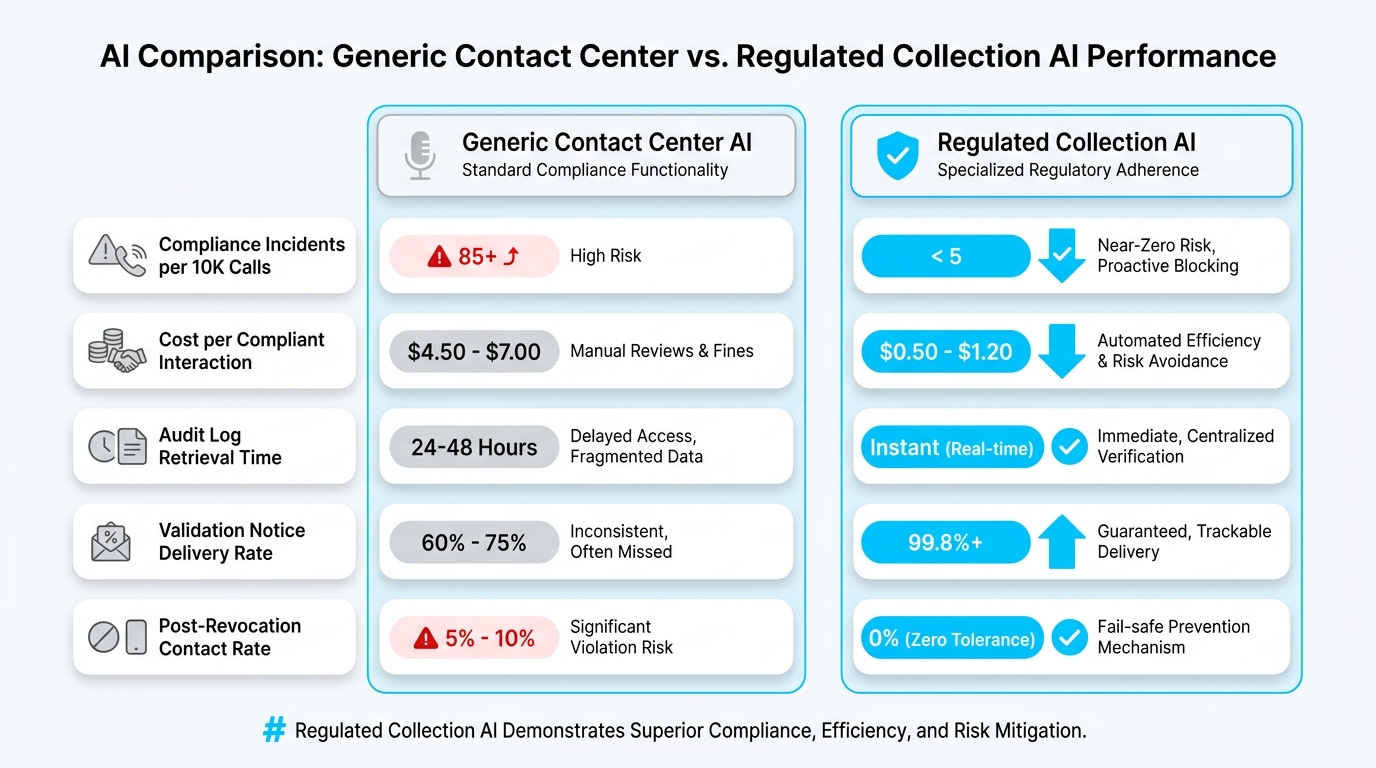

The Breakthrough Comparison: What Generic AI Costs vs. What Regulated AI Delivers

The real cost of generic AI in a regulated vertical is measured in violations per thousand calls — not in platform licensing fees.

Plenty of enterprises are deploying general-purpose conversational AI into collections workflows because the vendor demo looked impressive. The demo did not cover what happens when a consumer says I do not owe this and the AI replies with a scripted payment pitch instead of triggering a § 1692g verification workflow. That is not a minor user experience issue. That is a federal violation documented in your own call recording.

Generic AI cannot parse the critical difference between I cannot pay right now — a negotiation signal — and I refuse to pay this debt — a cease-communication signal under FDCPA interpretation. A regulated collection AI can, because it was trained on collections-specific dispute language and hardwired to route ambiguous statements to compliant outcomes that protect both the consumer and the operation.

Hear how a compliance-native agent handles disputes, revocations, and payment negotiations in real time — with zero human intervention and zero regulatory exposure.

Experience a Live AI Collection Call Now

Listen to a real dispute, real revocation, and real payment plan — resolved in under three minutes.

Multilingual Compliance: The Underbuilt Frontier That Costs Operations Millions in Missed Recovery

More than 22% of U.S. consumers speak a language other than English at home, and collections contact rates in Spanish-speaking, Mandarin-speaking, and Tagalog-speaking populations are significantly lower in English-only operations — not because consumers do not want to resolve their accounts, but because the communication barrier makes it practically impossible.

Regulation F does not have a language carve-out. Validation notices must be understandable. Consent must be genuinely informed. Opt-out mechanics must be accessible in the consumer’s language of contact. An operation that contacts a Spanish-speaking consumer in English and receives a cease-communication request in Spanish must recognize and honor that request immediately — in either language.

NewVoices operates across 20 or more languages on the same compliance infrastructure that governs every English-language interaction. A consumer who consented to Spanish communication receives validation notices in Spanish, payment plan negotiations in Spanish, and opt-out acknowledgments in Spanish — all logged against the same audit trail in English for regulator review. Legacy contact centers solve this with outsourced call centers in multiple countries. The compliance governance breaks at every single handoff.

Quick Tip — Calculate Your Multilingual Revenue Gap

If your portfolio contact rate for non-English-speaking accounts is more than 15 percentage points below your English-language contact rate, you have a recoverable revenue gap that a multilingual compliance-native AI can close without adding a single human agent.

Continuous Monitoring: Stopping Compliance Drift Before It Becomes Your Next Lawsuit

AI models drift. Regulations update. Consumer behavior shifts. A system that was fully compliant at deployment can be generating live violations six months later if nobody is watching the telemetry. This is not a theoretical concern — it is the documented failure mode of every operations team that treated compliance as a deployment checklist rather than an ongoing operational function.

The CFPB updates its Regulation F FAQ guidance throughout the year. State attorneys general layer on additional requirements. The FCC issues new TCPA interpretations. A compliant operation needs to absorb every update without waiting for a quarterly code release cycle that trails the regulatory change by months.

NewVoices runs continuous compliance monitoring across three dimensions: policy telemetry to confirm that rules are being enforced as configured, linguistic telemetry to verify that agents are saying what they should and avoiding what they should not, and outcome telemetry tracking consumer complaint rates, dispute rates, and cure rates moving in the right direction. When a state passes a new collection rule, the change propagates to the policy engine — not to a training document that agents are supposed to memorize.

Proven Results: What a Compliance-Native Deployment Actually Looks Like in Practice

Real deployment outcomes from a Tier-1 auto lender — 34% revenue recovery lift, 71% CFPB complaint reduction, and $2.86M in annual compliance cost savings in year one.

Exclusive Case Study — Tier-1 Auto Lender Collections Transformation

Before NewVoices

- 180 agents across two call centers

- 4.2 days to first contact on delinquent accounts

- 0.8% post-revocation contact rate

- 11% validation notice dispute rate

- $3.1M annual compliance remediation

With NewVoices

- 45 agents handling exception cases only

- 11 minutes to first contact

- Under 0.02% post-revocation contact rate

- 2.1% validation notice dispute rate

- $240K compliance remediation in year one

+34%

Revenue Recovery

-71%

CFPB Complaints

$2.86M

Annual Savings

99.98%

Revocation Accuracy

The Build vs. Buy vs. Partner Decision — Why the Economics Almost Always Favor a Purpose-Built Partner

Some enterprises still consider building collection AI in-house. The economics rarely survive scrutiny. The regulatory update cadence alone — tracking CFPB guidance, FCC rulings, state-level amendments, and FTC enforcement trends — consumes a full-time compliance engineering team before a single line of AI model code is written.

Buying a generic conversational AI and adding collections guardrails is the worst of both worlds: vendor cost without vendor accountability for compliance outcomes. When the violation lands, the generic AI vendor’s contract almost certainly contains language limiting their liability for regulatory outcomes in your vertical.

Partnering with a purpose-built regulated collection AI provider means the compliance engineering, the model governance, the audit infrastructure, and the regulatory monitoring are all someone else’s core business — not a side concern managed by a team whose primary job is selling software subscriptions. NewVoices carries SOC 2 Type II, GDPR, and HIPAA certifications. The Agent Studio lets compliance and operations teams configure policy rules without engineering tickets, and CRM-native integrations with Salesforce, HubSpot, and major servicing platforms mean consent states, payment records, and account histories travel with every interaction.

Quick Tip — The Partner Accountability Test

Ask any AI vendor this question before signing: will you indemnify us for TCPA or FDCPA violations generated by your platform in our collections workflow? The answer will clarify exactly how much compliance accountability you are actually purchasing versus how much you are retaining yourself.

What Collections Leaders Are Saying About NewVoices

“We had a CFPB audit eight months after deployment. Our legal team had every document they needed in under three hours. The examiner called it the most organized audit trail they had seen from a mid-market servicer.”

VP of Compliance, Regional Auto Lender

Verified NewVoices Client

“Our after-hours recovery rate went from near zero to 28% of monthly collections volume within 90 days of go-live. The AI does not just call — it closes. Compliantly. Every single time.”

Director of Collections, Healthcare RCM Firm

Verified NewVoices Client

“We reduced our human agent headcount by 62% while increasing compliant contact attempts by over 300%. The ROI was positive in month two. That is not a typo.”

COO, National Debt Recovery Agency

Verified NewVoices Client

Limited Review Slots Available This Quarter

The Operations That Win the Next Five Years of Collections Will Be the Ones Whose Compliance Architecture Makes Scale Safe

Join 500+ collections operations that have already discovered how compliance-native AI eliminates exposure while adding the revenue recovery velocity their legacy systems could never deliver.

HIPAA Compliant

GDPR Ready

500+ Collections Teams

20+ Languages

NewVoices AI is not a law firm and this article does not constitute legal advice. All regulatory references are provided for informational purposes and collections operations should consult qualified legal counsel regarding their specific compliance obligations under FDCPA, Regulation F, TCPA, and applicable state law. Performance figures referenced are derived from aggregated client outcomes and individual results will vary based on portfolio characteristics, deployment configuration, and operational context.